The AI Reality Check

Decoding the Application Layer

Billions of dollars are currently pouring into AI data centers, chips, and foundational models, but the ultimate test of that massive investment happens in just one place: the Application Layer.

In my last post, I mapped the architecture of the AI industry. Today, we are diving into the top of that stack to answer the industry’s most critical question: how do we separate the technological hype from real, sustainable economic value?

While all layers are important, I’d argue that at this point in time, the application layer is the most critical of all. The first reason is this is where theoretical value becomes real value. If social value isn’t created, why should anyone care about AI?

A second and related reason is this is where financial value is realized. Social value and financial value can be unaligned. When they are unaligned, society can miss opportunities and experience waste. This cuts both directions.

A third and also related reason is that as individuals we care about our own financial positions, and this layer’s financial performance will set limits on the financials of every other layer. If revenues can’t be generated here, they cannot pay off the investments already made and planned for model training, nor investments made and planned for data centers filled with AI compute capable chips.

The goal of this post is to understand those aspects. Where does (or could) revenue come from? How large are these flows, and what motivates or justifies them? In the process, we’ll learn more about how AI is changing the world today and in the future.

Who are the providers in the Application Layer?

The way I define it, the application layer will seem like it includes almost the entire industry. I’ll explain a model to differentiate the application layers of these organizations from their contributions to other layers.

At the forefront, we have the foundational model builders like OpenAI (with ChatGPT), Anthropic (with Claude), and Google (with Gemini). While they provide the underlying “Intelligence Layer,” they also act as direct-to-user application providers. Everyone wants to—and needs to—be in the application layer. All the core providers want to enable diverse users within the application layer, but cannot entrust their future solely to a developing ecosystem. They are thus both enablers and active participants.

Alongside them are the massive cloud platforms—most notably Microsoft and AWS. While it’s tempting to look at their packaged applications (like Microsoft Copilot), their true gravity in the enterprise space lies in platforms like Azure AI Foundry and Amazon Bedrock. These platforms provide the crucial API infrastructure that allows other businesses to build their own custom AI applications. Because of their sheer scale and their role in hosting these APIs, their movements dictate much of the financial reality of this layer.

This reliance on API infrastructure is perhaps the most common blind spot in the current AI discourse. Media pundits, the general public, and basically anyone not actively involved in building AI-enabled applications consistently overlook it. It’s easy to fixate on what is visible—the chat interfaces and packaged consumer tools. The enterprise API layer, however, operates quietly behind the scenes, routing data and powering internal corporate workflows. This infrastructure isn’t a secret; the documentation for Bedrock and Azure AI is entirely public. But because the average person has no reason to read it or interact with it, this critical financial and operational engine remains largely hidden from view, and will likely remain so.

Finally, beyond these hyperscalers and hidden API layers, there is a rapidly expanding ecosystem of AI applications. While pure-play startups (like Cursor, Midjourney, or Harvey) provide early examples of entirely new workflows built from the ground up, they represent just a fraction of what is possible. Ultimately, this layer is about embedding AI into existing processes and tools, making it generally pervasive over time, with many of the most transformative use cases yet to be realized.

The Consumer vs. Enterprise Split

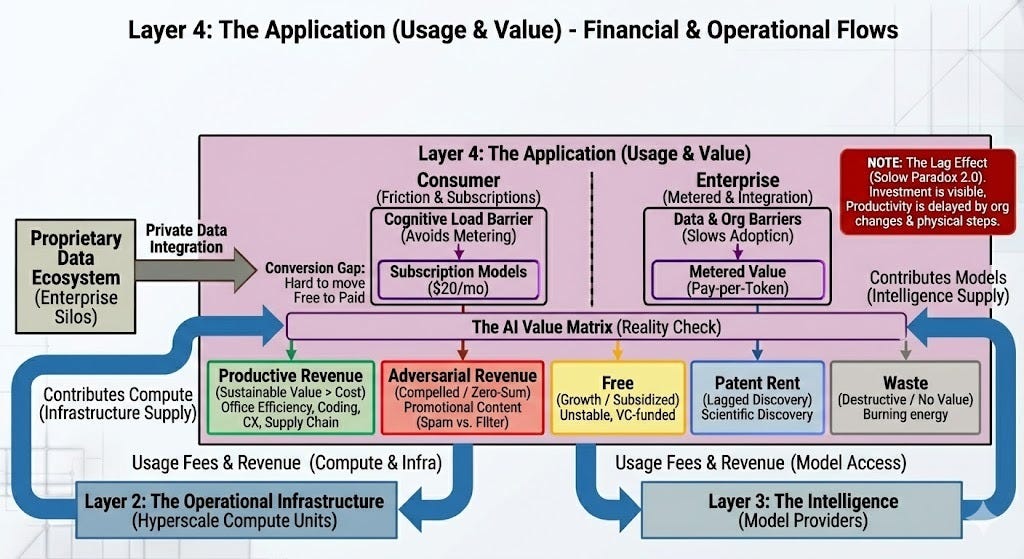

A key starting point to making sense of the application layer—and where its revenue comes from—is to categorize usage into two segments: consumer and enterprise.

The consumer segment encompasses personal usage, while the enterprise segment encompasses usage contracted for by a business. The lines can be blurry with self-employed businesses, gig work, and shadow enterprise usage. Imperfect as the distinction is, it still serves a purpose. The consumer segment shares dynamics regarding free usage and subscriptions that are important to understand potential growth. The enterprise segment is very diverse; while it has leading workload types, those workloads share pressures to demonstrate return on investment (ROI) and are challenged by implementation and integration.

Revenues for consumer usage are generally subscription-based. Conversion from free to paid is not straightforward; while limits on free usage create pressure, they can also alienate users. In this segment, usage isn’t measured by ROI but by “vibes”—does the user feel the tool is worth the monthly fee?

Conversely, the enterprise segment defaults to metered API usage (pay-per-token). This is exactly why the API platforms mentioned above (Bedrock, Azure AI) are so critical—they form the backbone of this enterprise business model. This metered structure creates a more predictable future by correlating revenue and costs directly. However, forecasting enterprise revenue depends on how capable organizations are at closing implementation and integration gaps. In a fully rational market, metered usage would create significant profit, but if the market deploys more capacity than the demand can satisfy, we may see usage sold at a loss just to recoup sunk costs.

The Activity Value Matrix

To truly answer the core questions of this article regarding social value, financial value, and financial performance, we need another framing tool alongside the consumer/enterprise split. This is where the Activity Value Matrix comes in.

The Activity Value Matrix is crucial because it establishes a reasoning model for what type of AI activity actually brings net-positive value back to society, versus activity that merely burns compute to propel the industry forward without creating real benefit. Furthermore, it helps us identify precarious gaps: cases where AI could create immense social value, but because we lack a sustainable revenue model to support it, that value will fail to materialize sustainably. By analyzing the relationship between Value (economic/social utility), Revenue (monetization), and Usage (active consumption), we can map the true health of the application layer:

From a social perspective, we have a few rows we prefer, but the most important is productive revenue. Free goods are enjoyable, but unsustainable, and so at a society level, we should expect to eventually pay. Public goods are likewise excellent, but the arrangements are complex and apply to fewer situations. While we might wish for an endless supply of free or public goods, it is via activities with productive revenue that we’ve moved forward.

Likewise, there are some rows we should fear. Waste is clear. The exploitative patent rent is clear. General patent rent is less clear. From a simple preference, we should dislike it. But patent rent is often a useful tool to promise as a privilege. When managed well, that promise encourages investment that subsidizes activity that creates growth that could not occur from productive revenue alone.

Moving Bottlenecks and Remnants

With these tools—the consumer/enterprise split and the Activity Value Matrix—we can start to examine individual use cases. Whether driven by consumer subscriptions or the pressure to recoup enterprise sunk costs, the operational reality is that actual AI adoption is heavily challenged by implementation and integration. As this adoption progresses, we will repeatedly encounter new bottlenecks.

Many bottlenecks are simply standard operational hurdles—like migrating legacy data, reorganizing teams, or passing compliance reviews—that get addressed one by one. While solvable, they still create significant diffusion delays that push the realization of productivity gains further into the future. Another type “remnants”, on the other hand, are the most resistant bottlenecks. They are the stubborn areas left behind after the easy problems are solved.

One of the most stubborn types of remnants is adversarial. As the matrix highlights under “Compelled / Adversarial Revenue,” these actions create a continuous loop of demand for intermediate outputs just to maintain existing outcomes—like AI generating better spam, which requires better AI to filter that spam. This burns energy and resources, generating revenue and usage, without creating net-new social or financial value.

To see how these bottlenecks and remnants shape an industry, consider Coding—arguably the leading edge of the application layer. Software developers are culturally accustomed to disruption, which reduces the organizational friction and diffusion delays seen elsewhere. Yet, their use cases perfectly map to our frameworks:

Responding to the Adversarial First: A wave of security related investment is underway, and I expect will accelerate. This early adoption is driven by compelled security needs—using AI to find vulnerabilities and harden systems before attackers can use AI to exploit them.

Paying Down Debt: AI is being deployed to clear existing bottlenecks by paying down technical debt—modernizing deprecated platforms and freeing up locked capital.

An Engine for Change: Because software underlies modern business, increasing developer productivity acts as an engine for change across all other industries, eventually translating to new productive revenues.

However, if development capacity isn’t solved first, consider how a bottleneck might manifest as an increasing “Proposal-to-Product” ratio. If AI halved the time needed to create software feature proposals of twice the quality, we might describe it as a 400% efficiency improvement. We might also see twice as many proposals. However, if the capacity to actually write the software hasn’t increased proportionally, that 400% internal productivity boost might only translate to a 10% increase in final value.

If we’re not careful, we might incorrectly diagnose the proposal process as the problem. We might even blame AI and suggest all of those new proposals were “AI slop”. While it’s possible for tools to be misused, it would be ironically sloppy to jump to that conclusion. The overuse of AI slop is already a problem, so we should not add to it. If users decrease their effort by 10x, and get half the quality, then yes, we can call their output slop. But that would have been true if they decreased their effort by half without tools.

The real story here is of the bottleneck. The unused proposals aren’t necessarily low-quality slop; they are simply piling up behind a bottleneck further down the line.

Conclusion: The Reality Check

The Application Layer is the industry’s “Reality Check.” While the lower layers (Compute and Intelligence) have seen massive investment and technical breakthroughs, the Application Layer is where those breakthroughs are forced to justify their existence.

The distinction between the Consumer and Enterprise segments is vital to this justification, as it dictates the very survival of business models. In the consumer world, the value is personal and often ephemeral, driven by individual preferences and “vibes.” Here, adoption can be viral and instantaneous, but loyalty is fickle and valuations are tied to user engagement. In the enterprise world, value is rigorous and must survive the gauntlet of organizational change and ROI calculations. While adoption is slower due to integration hurdles, the resulting business models are often more durable and command higher valuations based on proven efficiency gains. While many use cases—like coding or creative generation—will exist in both segments, they will take on different “shapes” and adoption velocities based on these divergent preferences.

As we look forward, the specific tasks—the “Use Cases”—will define which segment wins and how much of that massive investment in lower layers can actually be recouped. In my next post, we will dive deeper into the Activity Value Matrix to see exactly where this “productive revenue” is hiding, how the shapes of use cases shift between consumer and enterprise, and where energy is simply being burned as “waste.”

The Architecture of a Gamble

A while back I talked about producing an analysis of the AI industry. I’ve put together something pretty extensive, but on reflection, I’ve decided to put it out in multiple parts. This post today functions more as an outline, where the following posts will dive more into each layer of this stack and then finally look in more depth at the macro-economic aspects.

The Slop Scapegoat: AI

I don’t like the term “AI slop”. As a term it’s used far too casually. The Internet has had copious amounts of slop for a while, if we describe slop as low-quality material created to grab eyeballs. For example, the article-spinning software of the 2000s, content farms churning out SEO-driven articles, or the rise of viral clickbait. Quantity over quality, you might say.