The AI Jobs Blind Spot

Why Job Creation is the Default

When discussing AI and the future of work, there is a glaring blind spot in the general discourse: the fundamental baseline state of an economy is to create new jobs.

It is common to hear people argue that “technology creates new jobs,” usually pointing out that despite centuries of technological advancement, nearly everyone is employed today. Therefore, they argue, the fear that technology destroys jobs must be wrong. While it is true that technologies can both create and eliminate specific roles, framing the debate entirely around the technology misses the underlying engine. The real topic is the economy itself, which naturally seeks to create new jobs from available resources—the most limited of which is labor. Whether ATMs create more or less demand for bank tellers is simply not as important as we think.

Debates about automation often get stuck here. One side correctly argues that economies have historically created new jobs, but incorrectly attempts to prove this by claiming technologies always create new jobs. These are two different arguments. This minor framing issue does a lot of heavy lifting in keeping both sides from understanding each other. Once you look past the technology and focus on the economic engine, you can discuss the future of jobs in far more effective ways than debating the fate of bank tellers.

Why Does an Economy Create New Jobs?

It is easy to misunderstand how economies work if you view them through a lens of strict limits rather than dynamic balance. A certain mindset approaches every economic issue as a zero-sum game of apportionment—assuming there is a fixed number of jobs in the world, and introducing a new technology either adds to or subtracts from that finite pool.

It is not hard to see why this mindset takes hold; in a moment-to-moment sense, it appears true. At any given second, there are a fixed number of jobs. Eliminate 500,000 of them instantly, and you have 500,000 unemployed people. But economies are not static moments; they are moving systems that perpetually seek equilibrium. While external limits exist, the internal machinery of an economy is entirely dedicated to finding a balance between those limits and the limitless preferences and desires of the people within it.

That is why, in their default state, economies always create new jobs out of available labor. If there is an unmet desire among the population, and there is labor available to fulfill it, the economy will generate an opportunity to put that labor to work. This balancing act isn’t instantaneous. There is a “seeking” process to find a new equilibrium. Sometimes this process stalls, the economy malfunctions, and we experience high unemployment. But high unemployment is not the result of an absolute limit on total possible jobs; it is a breakdown in how quickly the economy adjusts to new parameters.

Will AI Create New Jobs?

Yes, it will. Will it create more than it eliminates? Probably not. But the economy will still create new jobs, and it isn’t dependent on AI to do so.

Consider software engineering. The number of computer programmers necessary to write and maintain a specific piece of software will likely go down due to AI. However, that doesn’t extinguish the societal desire for more software or better software. AI didn’t create those desires, but those human desires will inevitably create new jobs focused on building that better software.

Economies do not constrain the matching of human desire and available labor to a specific job description. Often, one job type is entirely replaced by another. As farming became more efficient with the advent of tractors and fertilizers, freed-up labor initially went back into farming to manage more land. Eventually, agricultural limits were reached, a different source of balance was invoked, and that freed-up labor transitioned into industry and manufacturing.

The same principle applies to AI. Until every need and desire of the human population is met, there will be pressure on the economy’s balancing forces to create jobs to meet them. The only absolute barrier to meeting that pressure is a lack of available labor. If AI ever becomes so universally capable that humanity literally has no more unmet needs or desires, we will have reached an incredibly unprecedented state. While I have previously explored how the economy might actually function if that AGI future arrives, history tells us that this kind of post-scarcity utopia is always further away than we imagine. In the meantime, the world gets more efficient without flipping into a topsy-turvy reality where the fundamental economic force of putting available labor to work ceases to exist.

The Economic Future from and of AI

This will be part one of a two part series. In the first part, I want to outline some of my views about how salient a set of what we might call existential concerns about AI should be. In part two, I want to discuss some more immediate interactions with today's economy

What About the Short Term?

These macroeconomic forces dictate our long-term expectations: the economy will eventually balance out. But we live in the present, making it entirely reasonable to ask how the job market is changing right now and what to expect in the short-to-medium term.

Currently, I find the evidence of broad job market changes already caused by AI to be very weak. Conversely, I find the probability of broad future changes to be very strong. Most informed observers without ulterior motives tend to agree with this assessment. However, the prevailing public narrative has settled on the exact opposite amalgamation.

To the casual observer, the dominant narrative is that AI has already triggered widespread job losses and restructuring, but will ultimately fail to live up to its long-term hype due to inherent technical limitations. While this is just a prevailing vibe—and conversations often reveal more nuance—it is worth examining how illogical this combination of opinions is, and why it is so easily adopted.

Weighing the Evidence for Changes Already Occurred

The belief that AI has already upended the job market is easy to support because countless articles have delivered it as a concrete conclusion.

One form of article takes real statistics about a weakening job market—or specific sectors like tech—and correlates them directly with the release of AI products like ChatGPT. As a hypothesis, this is fine; as a conclusion, it is incredibly poor. It fails for two main reasons: it ignores major alternative economic forces, and it assumes a timeline of corporate reaction that defies reality.

Because an economy is about balance, if other substantial forces can explain job market shifts, the “AI did it” correlation becomes incredibly weak. When looking at the period since ChatGPT’s release in late 2022, we are swimming in alternate economic forces.

First, the COVID-19 pandemic created a profound shock. In-person jobs vanished and slowly recovered, while tech firms over-hired to meet the surging demand for remote work, supply chain management, and digital education. Executives extrapolated that temporary surge into permanent future demand. While some of that expected permanent shift was indeed realized, the world largely returned to a physical “normal.” As the most extreme growth expectations evaporated, it triggered a sharp, ongoing correction in tech employment.

Second, we experienced a severe inflation surge. While the exact interplay is complex, the relationship between inflation, interest rate hikes, and employment cooling is a foundational and uncontroversial economic reality. Finally, we are running the radical experiment of applying 1930s-style tariffs to a modern, globalized economy. Disentangling these three major, structural forces from the data to pinpoint AI as the primary culprit for recent layoffs is nearly impossible.

Furthermore, the timeline required for these correlation theories is implausibly fast. ChatGPT is released, and supposedly, jobs immediately begin to decline. No economic theory predicts immediate structural decline from a new tool. At a minimum, users must adopt the tool and prove its efficiency. Then, managers must recognize this efficiency, rewrite staffing plans, get approval, and execute layoffs. This takes quarters, if not years. Yet, the main correlational narratives point to tech job losses that actually began months before ChatGPT was even released.

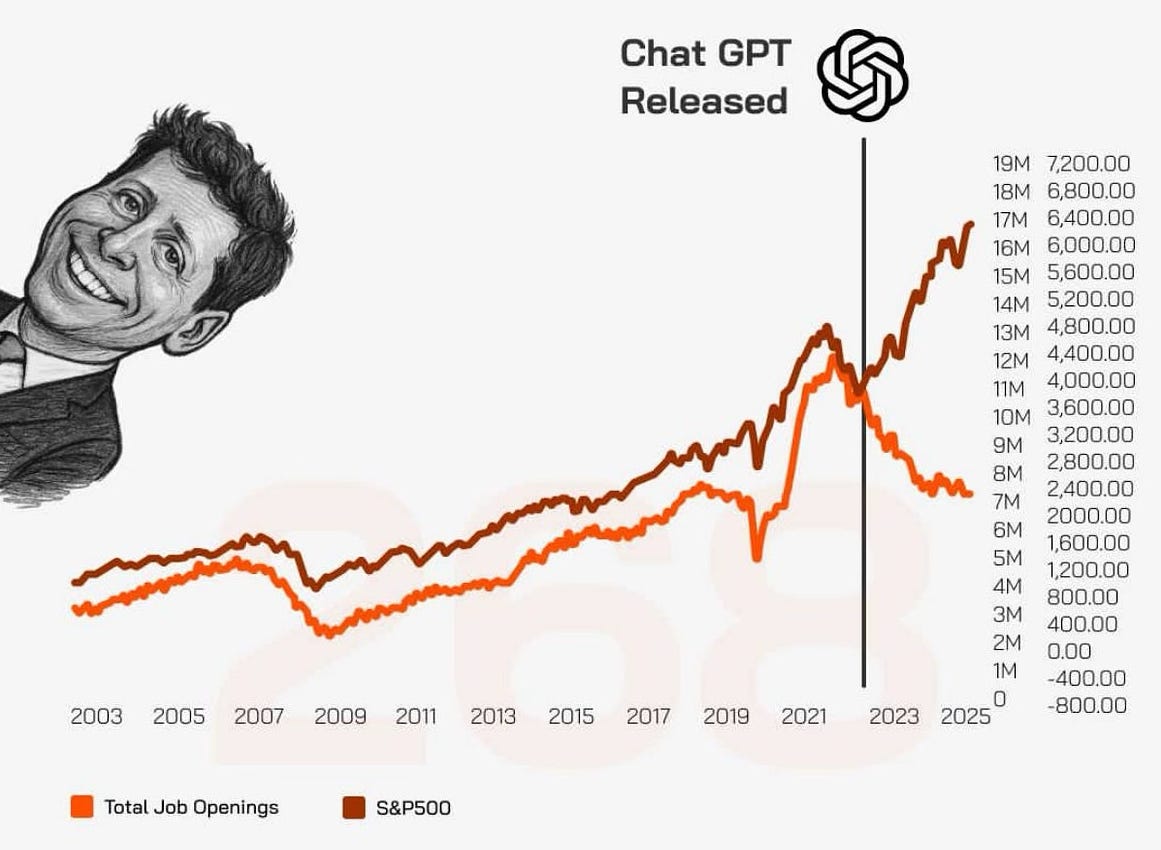

This exact flawed logic was perfectly encapsulated in a viral graph that circulated widely, which Derek Thompson observed was often being shared with commentary declaring it the "scariest chart in the world". The chart accurately shows the S&P 500 rising while total job openings fall, with an ominous vertical line marking ChatGPT’s release right at the inflection point.

While the data points themselves are factually accurate, the suggested correlation is a classic case of confusing coincidence with causality. As a piece of media narrative, it is highly persuasive; as an economic argument, it is entirely unsupportable, especially considering the downward trend in job openings clearly begins before the AI tool was even available to the public.

It is entirely possible that some executives are acting on the ‘vibes’ of AI, restructuring their companies in anticipation of future gains we can’t yet see in the data. But in the present moment, those ‘vibes’ serve as the perfect smokescreen. Whether an executive is genuinely anticipating an AI revolution or simply needs to fix a bloated balance sheet, the public narrative sounds exactly the same. In reality, managers claiming AI-driven layoffs rarely have the data to back it up; rather, they have ulterior motives for cutting staff that they prefer to keep hidden.

Hyperscalers and major tech firms do not want to discuss how their cash flow is being squeezed by the massive capital expenditures required to build data centers and hoard Nvidia chips. Highlighting that reality invites investor scrutiny regarding the ultimate return on those investments. It is much easier to feed the market a narrative of “AI efficiency.”

Then you have executives who simply mismanaged their companies and need a convenient scapegoat for the necessary corrections. Add to this the universal motivation of any executive looking for a short-term stock boost: announcing headcount reductions under the guise of “doing more with less” is a brilliant Wall Street narrative. This practice of “AI-washing” layoffs—as seen with Jack Dorsey’s recent cuts at Block—avoids calamitous explanations like “we are losing customers” or “we are running out of money,” and actively excites investors in the short term, even if the cuts hollow out the company’s long-term capabilities.

Whether a company can actually do more with less will be tested in the future, not the present. The popular narrative assumes that newfound efficiency naturally dictates layoffs, but for a healthy company with opportunities to grow, turning efficiency into layoffs is hugely damaging. If a company suddenly needs fewer resources to maintain its current output, the logical move is to redeploy those resources to capture more market share or build new products. Layoffs generally only make sense if a company is correcting a past mistake (like rampant over-hiring) or if it has exhausted its growth options.

This reality exposes two fundamental flaws in the current public discourse. First, extrapolating the actions of these shrinking companies to the entire economy leaves no room for the story of companies that will use AI to expand. Second, it means these opportunistic, short-term cuts will eventually have to be reversed for companies that actually do have future potential. If they cut too deep today, service quality will degrade, feature releases will slow down, and competitors will steal market share. Eventually, they will be forced to reverse course and re-hire to regain their footing—having needlessly sacrificed their growth momentum for a temporary Wall Street bump. By then, however, the executive will have likely kept their job, exercised their stock options, and enjoyed the short-term bump from the AI narrative.

Another form of article driving the public narrative simply repeats these executives’ statements verbatim. They do so without examining the underlying data or considering the obvious financial incentives for executives to spin bad news (over-hiring or cash flow issues) into a forward-looking story of AI-driven efficiency.

The Delusion of Immediate Efficiency

Accepting these narratives uncritically builds a dangerous delusion: that AI has already unlocked massive efficiency gains, that the best use of those gains is shrinking the labor force, and that companies failing to do so are falling behind.

In reality, while AI has added efficiencies in specific pockets, we are mostly still in the learning and adoption phase. Any hours saved are frequently counterbalanced by training, integration, and implementation costs. Where true, systemic efficiency has been achieved, it is very recent and far from pervasive.

Because this shift is so nascent, we don’t yet have stories of mature firms using AI to successfully expand. Aside from new startups or companies explicitly selling AI infrastructure, the narrative is entirely dominated by contractionary stories—which, as established, are largely misdirection. Accepting these false contractionary tales severely distorts our perception of what the technology is actually doing to the economy.

Non-Linear Transitions

Furthermore, we must remember that stories about the impact of a specific technology are not comprehensive stories about the entire economy. If employment in a field like insurance claims processing genuinely contracts due to AI, the compensating job expansion will not necessarily be AI-related at all.

Freed-up labor might allow housing construction to expand, making homes more accessible and lowering costs. While expanding the housing industry requires more than just available labor (like zoning reform or lower interest rates), if those external limits are removed, the economy will naturally funnel available labor toward that unmet demand. This kind of non-linear adjustment is exactly what dynamic economies do. It is rarely instantaneous, and it is never without friction, but in its default state, the economy makes the adjustment.

A common objection here is the “skills mismatch”—the idea that a laid-off insurance claims processor isn’t going to suddenly start swinging a hammer. But an economy does not rely on perfect one-to-one transitions. Labor markets are highly dynamic, and indirect shifts do most of the heavy lifting. While some claims processors might actually enjoy learning a trade or already have prior experience in one, it is far more likely that their existing skills shift adjacently. An insurance adjuster might transition to a construction firm as a project manager, which in turn frees up the multitasking owner to spend more time actually building.

Even if only a small proportion of the labor force makes these types of lateral moves, the cascading effect absorbs vast amounts of economic change when all the different pathways are added up.

Conclusion

Ultimately, the story about the future of jobs is incomplete without an understanding of this economic dynamism. AI is a profound technological shift, and when the really significant changes it promises do start happening, that dynamic adjustment process will become more obvious.

But right now, separating the noise of the current moment from the signal of long-term economic behavior is crucial. If we believe media narratives driven by ulterior corporate motives, we will confuse ourselves with expectations that are neither complete nor correct. We must remember that AI is just a tool; the economy is the engine. As long as human desires remain unmet, the economic engine will continue to do what it has always done: take available labor and put it to work.

I think you are on the right track with this post. You and your readers might want to look at the late William Baumol's Yale University Press (2012) book The Cost Disease, which develops some of the ideas about technical change and the level and composition of employment in more detail.